Categories

Market UpdatesPublished May 13, 2026

Austin Market Update - May 2026

AUSTIN MARKET UPDATE

May 2026

What's really happening in the economy, and what it means for your home.

From Schuyler Williamson, Williamson Group Real Estate

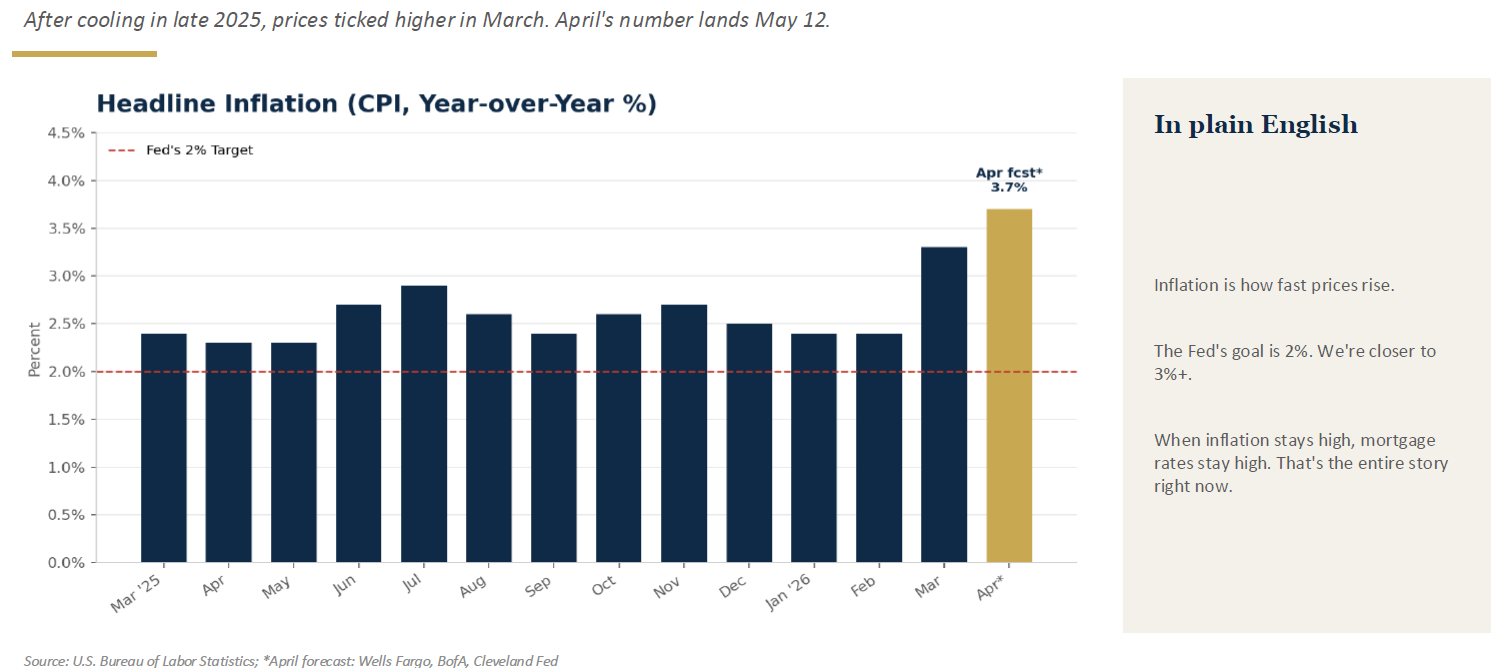

Inflation Is Calling the Shots

One number matters more than anything else this month. On May 12, the Bureau of Labor Statistics releases the April Consumer Price Index. CPI is the official measure of how fast everyday prices are rising. It drives Fed policy, and Fed policy drives mortgage rates.

• When CPI runs hot, the Fed keeps rates higher to cool things off.

• Higher Fed rates equal higher mortgage rates equal less affordable homes.

• Cooler CPI works the other direction: lower rates, more affordable payments.

March CPI came in at 3.3%, the highest reading since May 2024. Wells Fargo and Bank of America are forecasting April between 3.7% and 3.8% on the headline number, with core inflation (the steadier figure that excludes food and energy) at 2.7% to 2.9%.

Rates are not trending right now. They are reacting. CPI weeks create short windows where rates dip, sometimes for only a few days. Buyers who are pre-approved and ready to write an offer are the ones who win during those windows.

Why Inflation Won't Fully Cool: Oil

Inflation has been stubborn for one main reason. Oil.

• WTI crude is sitting near $98 a barrel, up from about $73 in early February.

• The conflict in the Middle East and the ongoing disruption of the Strait of Hormuz are keeping oil elevated.

• Higher oil prices push diesel prices higher, which raises the cost of shipping every product in the country. Those costs show up at the cash register.

• Cease-fire talks are underway. Any real progress there pulls oil and inflation back down.

Watch the oil price. It is a leading indicator for where inflation and mortgage rates are headed.

The Big Picture

Three numbers I check first every month:

• GDP: 2.0% growth in Q1 2026. Healthy and steady.

• Unemployment: 4.3% in April. Still historically low. Employers added 115,000 jobs, nearly double what economists expected.

• Inflation: 3.3% in March, with April expected at 3.7% to 3.8%. The Fed wants 2.0%. We are not there yet.

The economy looks healthy from a distance, but it does not feel stable. Strong jobs plus stubborn inflation plus global tension equals a Federal Reserve that wants to cut rates but cannot yet.

The Fed Is Changing Hands

Jerome Powell wrapped up his final FOMC meeting as Federal Reserve Chair in late April. Kevin Warsh, nominated by President Trump, is set to take over. Warsh has made it clear he wants to lower interest rates. The 12-person Fed committee is not unanimously on board, and several members have publicly pushed back.

Here is what markets are pricing in right now:

• Just a 17% chance of any rate cut in 2026, down from 62% in January.

• A small but real chance the Fed actually raises rates again later this year.

• Most major banks (JPMorgan, Wells Fargo) expect either zero cuts or one quarter-point cut by year end.

Don't make a housing decision on the hope of a rate cut. Make it on the math of today's payment, with a plan to refinance later if rates fall.

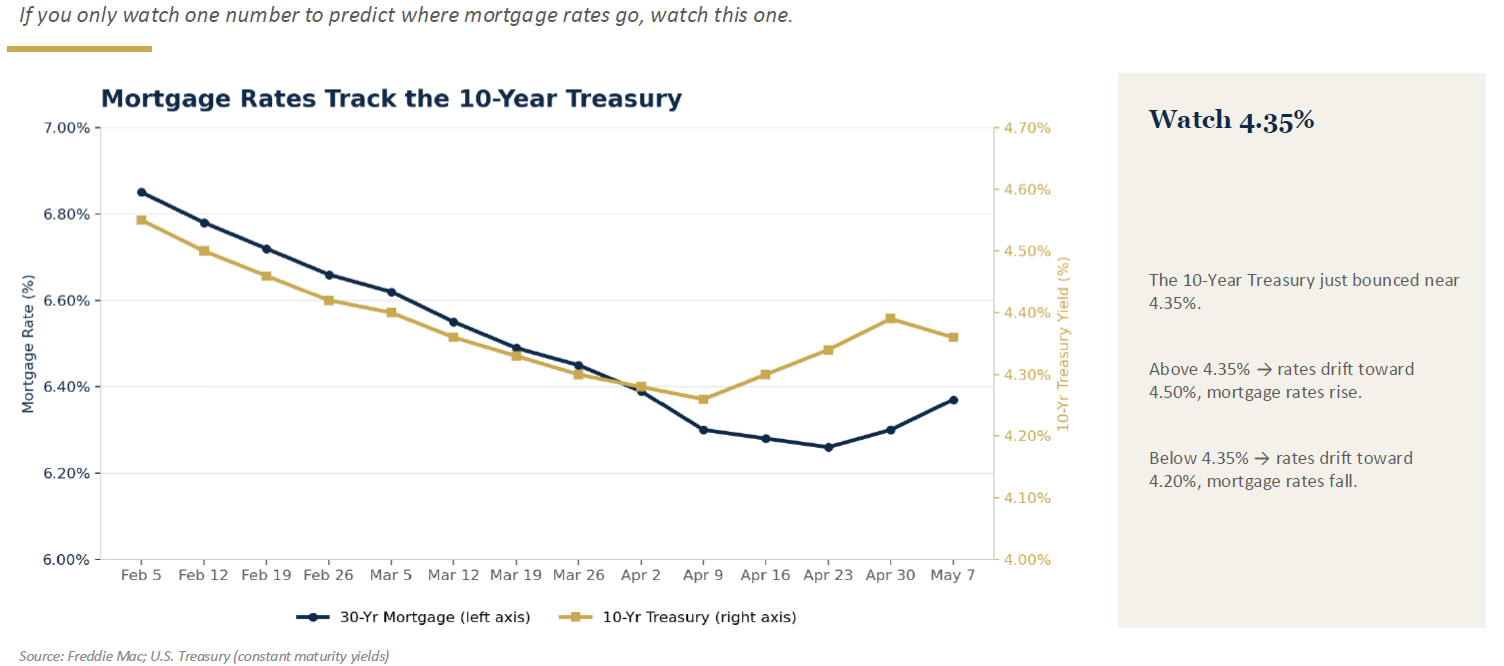

Mortgage Rates: Stuck in the Mid 6s

The 30-year fixed mortgage rate ended last week at 6.37% according to Freddie Mac, up slightly from 6.30% the week before. A year ago, the same loan was 6.76%, so we are meaningfully better year-over-year. We have been sideways for months.

If you only watch one number to predict where mortgage rates are headed, watch the 10-Year Treasury yield. Mortgage rates follow it closely.

• The 10-Year Treasury closed near 4.36% on May 7, after briefly spiking above 4.44%.

• If the 10-Year breaks above 4.35% and stays there, mortgage rates likely drift toward the high 6s.

• If it slips back under 4.20%, expect mortgage rates to ease into the low 6s.

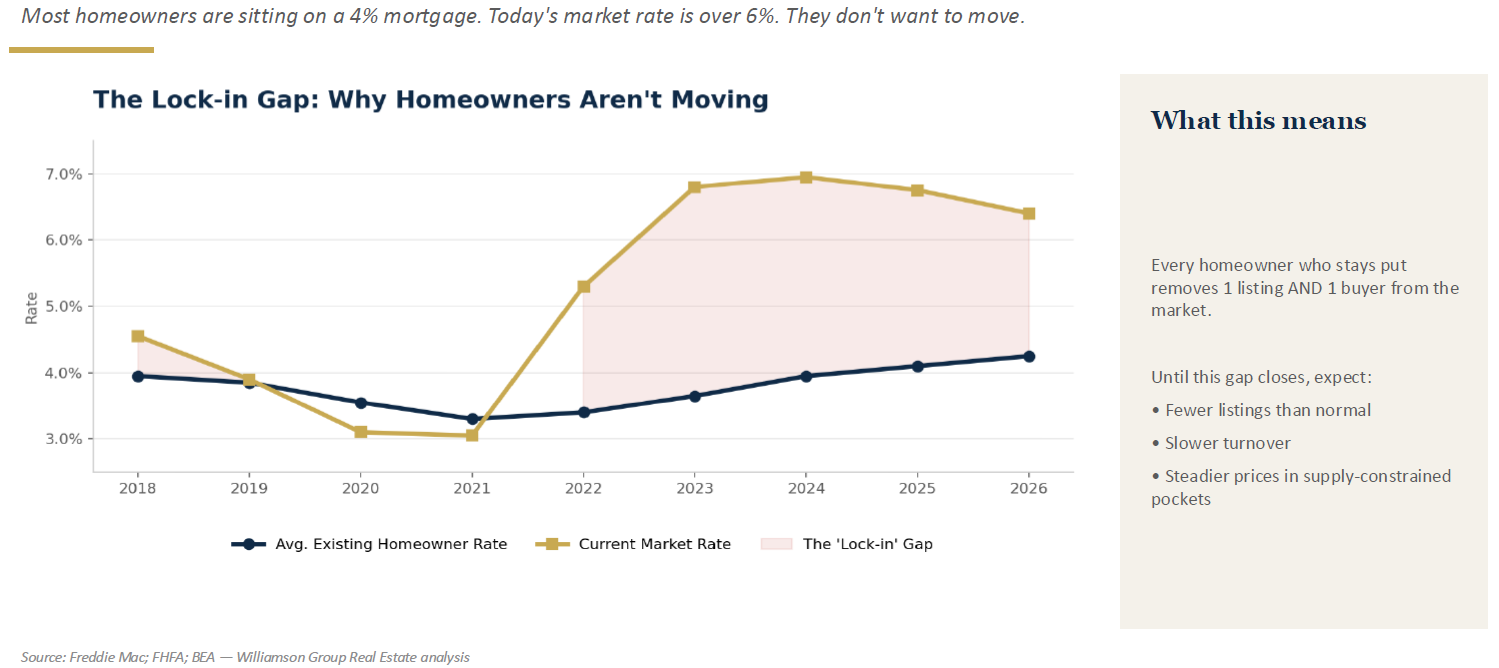

The Lock-in Effect: Why So Few Homes Are Hitting the Market

The average existing American homeowner has a mortgage rate of roughly 4.25%. The average new market rate is 6.40%. That is a 2.15% gap. On the same house, it means a payment that is hundreds of dollars higher.

Homeowners are doing the natural thing. They are staying put. Every time someone chooses not to move, two things happen:

• One less home gets listed for sale.

• One less buyer enters the market on the other side.

That is why turnover is so slow nationally. The gap will close eventually. Probably not in 2026.

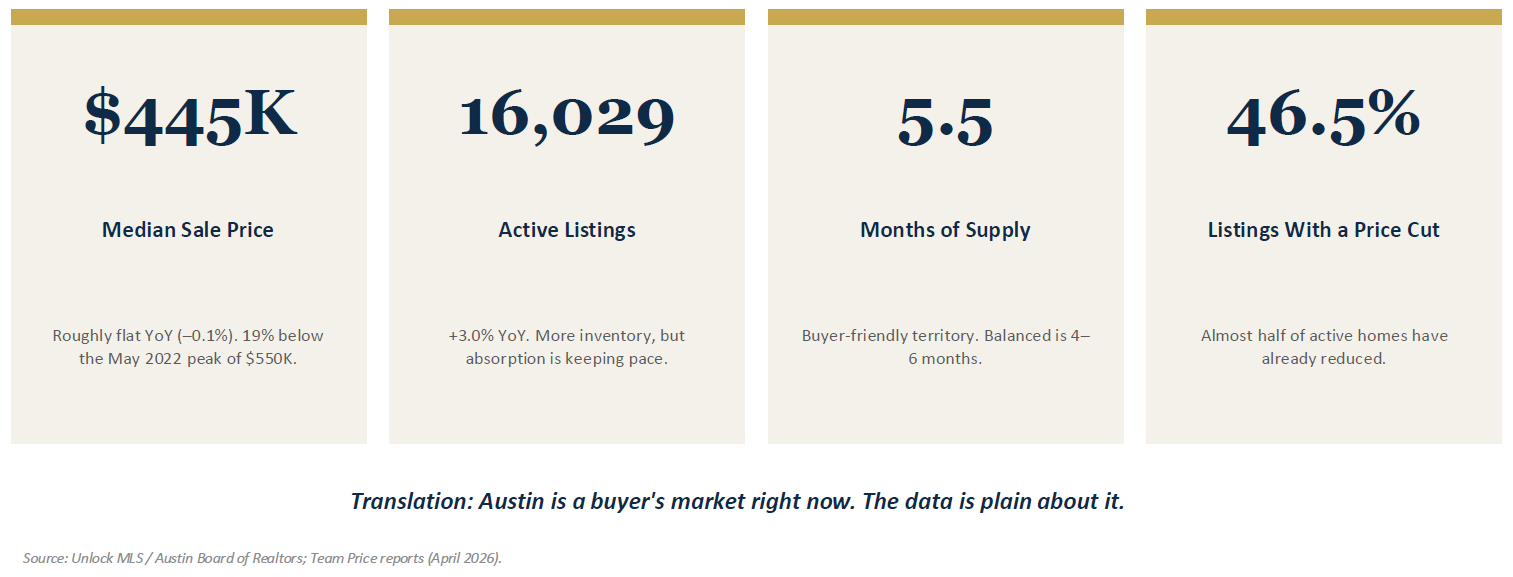

The Austin Market in May 2026

Local matters more than national. Here is the Austin snapshot from April 2026, sourced from Unlock MLS and the Austin Board of Realtors:

• Median sale price: $445,000. Essentially flat year-over-year at -0.1%. About 19% below the May 2022 peak of $550,000.

• Active listings: 16,029. Up 3.0% from this time last year. Buyers have more to choose from.

• Months of inventory: 5.5. Firmly in buyer's-market territory. Balanced is 4 to 6 months. Over 6 is a strong buyer's market.

• Days on market: roughly 85 days. Homes are not flying off the shelf. They are being shopped carefully.

• Listings with a price cut: 46.5%. Nearly half of every active home has already lowered its asking price.

• Pending sales: up 2.9% year-over-year. Buyer activity is real, just selective.

• Above-list-price closings: jumped from 13.1% to 16.3% in a single month. The right homes, priced right, still spark competition.

We are in a buyer's market. We are not crashing. Prices have held in a tight band for over a year. We have stabilized.

Why Austin Is Different from the Rest of the Country

Most U.S. metros are roughly flat in price right now. Austin is one of the few that has gone through a real correction.

• From 2020 to 2022, we had one of the fastest home-price run-ups in U.S. history.

• During that same boom, we built a lot of housing. Apartments, build-to-rent, single-family.

• When rates rose and demand cooled, all of that supply hit a slower market.

• The result: we have given back about 19% from the peak. The correction is mostly behind us.

Austin is no longer falling. It is stabilizing. That is a meaningful change from where we were in 2023 and 2024.

Central Austin: The Core Six ZIP Codes

If you live in or care about central Austin, here are the rough April 2026 medians for the six core ZIP codes:

• 78703 (Tarrytown, Clarksville): ~$1.35M. About 3.6% below last year.

• 78704 (South Congress, Bouldin, Travis Heights): ~$799K. About 2.5% below last year.

• 78731 (Northwest Hills): ~$1.05M. About 4.2% below last year.

• 78746 (West Lake Hills, Rollingwood): ~$1.66M. About 2.9% below last year.

• 78756 (Brentwood, Crestview): ~$720K. About 3.1% below last year.

• 78757 (Allandale, Crestview North): ~$690K. About 1.8% below last year.

Across all six, the pattern is the same. Small, single-digit drops year-over-year. That is a soft landing. The central core is doing what the broader Austin market is doing, just at a higher price point.

If You Are Buying Right Now

• You have leverage. Use it. Negotiate price, closing costs, and a seller-paid rate buydown.

• Do not wait for the perfect rate. Buy the right home today and refinance later.

• You can refinance the rate. You cannot go back and buy at today's price.

• Be ready to move on the right home. Feel free to pass on the wrong one.

If You Are Selling Right Now

• Price right on day one. Buyers are patient and will not chase you.

• Almost half of active listings have already cut price. Do not join them.

• The first 14 days of a listing produce more activity than weeks 3 through 10 combined. Do not waste them with an aspirational price.

• Presentation matters more than ever. Clean, staged, well photographed, priced at the market.

The Bottom Line

This is a unique market. Strong economy. Elevated interest rates. Patient buyers. More realistic sellers. That combination creates real opportunity for the people who understand what is happening.

The winners in this market are not waiting. They are the ones with a clear plan.

Buyers win by being patient and disciplined. Sellers win by pricing right from day one. Both win by understanding the market instead of reacting to headlines.

If you are thinking about a move this year, whether buying, selling, or just running the math, let's put a plan together. That is what I am here for.

Schuyler Williamson

Williamson Group Real Estate

Sources

• Unlock MLS and the Austin Board of Realtors, monthly market reports (April 2026).

• U.S. Bureau of Labor Statistics. Consumer Price Index (March 2026), Employment Situation (April 2026).

• U.S. Bureau of Economic Analysis. GDP (Q1 2026 advance estimate).

• Freddie Mac. Primary Mortgage Market Survey, week ending May 7, 2026.

• TradingEconomics, CME FedWatch, Mortgage News Daily, Wells Fargo, BofA, Cleveland Fed (CPI nowcast).

• Team Price Austin Real Estate Briefings (April 2026).

Schuyler Williamson

MBA , Realtor & Team Lead | Williamson Group Real Estate | Keller Williams Realty | PLACE

or another way